Resilience of industrial production amid uncertainty

Industrial production accelerated to a six-year high in the first half of 2026, supported by strong manufacturing growth, rising investment, and improving business conditions.

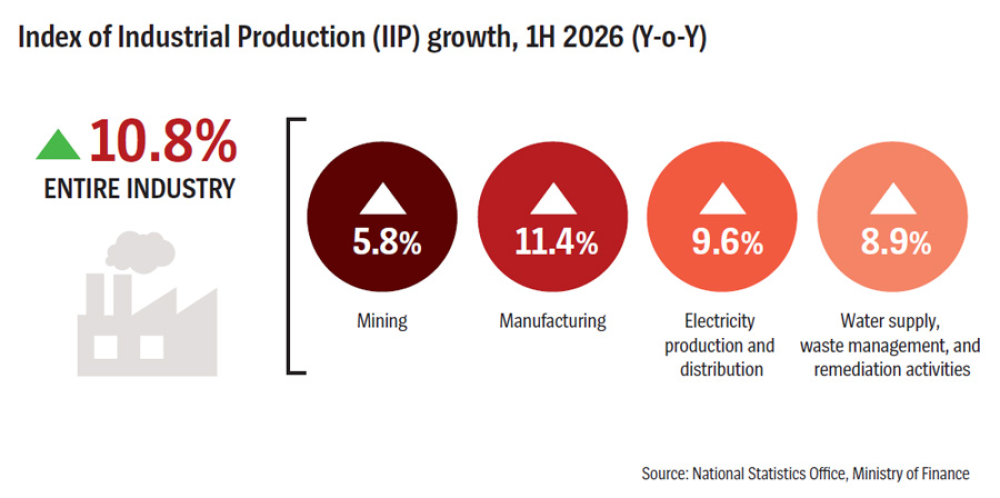

The latest data from the National Statistics Office (NSO) at the Ministry of Finance shows that Vietnam’s Index of Industrial Production (IIP) is estimated to have risen 11.2 per cent year-on-year in the second quarter of 2026. For the first half, the IIP expanded 10.8 per cent against the same period last year, up from 8.7 per cent in the first half of 2025 and marking the strongest first-half growth since 2019.

Industrial momentum

Manufacturing remained the main driver of industrial expansion, growing 11.4 per cent year-on-year, up from 10.5 per cent a year prior and contributing 8.9 percentage points to overall IIP growth. The sector benefited from stronger supply chains and rising demand from both domestic and export markets.

Electricity production and distribution increased 9.6 per cent, compared with 4.1 per cent in the same period of 2025, contributing 0.9 percentage points. Water supply, waste management, and wastewater treatment expanded 8.9 per cent, adding 0.1 percentage points, while mining rebounded with 5.8 per cent growth after contracting 3.5 per cent a year earlier, and also contributed 0.9 percentage points.

At the detailed industry level, several segments posted robust double-digit gains. Basic metals led the way, with growth of 21.5 per cent, followed by motor vehicle manufacturing with 17.7 per cent and beverages with 15.4 per cent, reflecting stronger consumer demand and higher utilization of production capacity.

Chemical manufacturing rose 14.8 per cent, non-metallic mineral products 14.9 per cent, and fabricated metal products 13.9 per cent, signaling accelerating infrastructure and construction activity that is driving demand for industrial materials and support industries. Traditional industries such as food processing and furniture manufacturing also maintained growth of more than 11 per cent, supporting agricultural value chains and domestic consumption.

Not all sectors exhibited the same momentum, however. Leather and related products posted a modest 4 per cent increase, while coal mining contracted 5.7 per cent.

The NSO reported that the IIP increased in all 34 provinces and centrally-administered cities in Vietnam during the first half of the year. Strong gains were concentrated in localities with rapidly-expanding manufacturing and electricity production, while slower growth was recorded in those where manufacturing, mining, or power generation are weak.

Manufacturing leads FDI inflows

Manufacturing also remained Vietnam’s leading destination for FDI. As of June 30, newly-registered FDI in the sector reached $10.76 billion, accounting for 61.9 per cent of all newly-registered investment nationwide. Including both new registrations and additional capital to existing projects, total registered FDI in manufacturing stood at $17.91 billion, representing 63 per cent of total newly-registered and additional capital.

More significantly, disbursed FDI totaled an estimated $13.03 billion during the first half of 2026, up 11.2 per cent year-on-year and the highest first-half figure in five years. Manufacturing alone accounted for 82.6 per cent of disbursements, or approximately $10.76 billion.

The continued expansion of multinational manufacturers has brought not only capital but also technology transfer, stronger management practices, and higher production standards, strengthening Vietnam’s domestic supply chains.

Improving demand has also been reflected in stronger sales and healthier inventory levels. The consumption index for manufacturing increased 10.8 per cent in the first half, compared with 9.8 per cent a year earlier, indicating that market demand is keeping pace with expanding production.

As a result, the average inventory ratio declined to 82.2 per cent from 85.7 per cent in the first half of 2025. Lower inventories alongside higher production suggest manufacturers are operating more efficiently, freeing up working capital while avoiding excessive stock accumulation; an indication that growth is increasingly supported by underlying demand rather than inventory buildup.

Labor market conditions also continued to improve. As of June 1, employment at industrial enterprises was 3.1 per cent higher than a year prior. Employment at FDI enterprises rose 3.1 per cent, with 2.4 per cent growth in the private sector and 1.4 per cent at State-owned enterprises (SOEs).

Employment expanded 3.2 per cent in manufacturing and 3.8 per cent in water supply and waste management, reflecting business expansion to meet rising orders. Though mining employment fell slightly, the industrial sector as a whole continued to play a critical role in job creation, supporting household incomes and consumer spending.

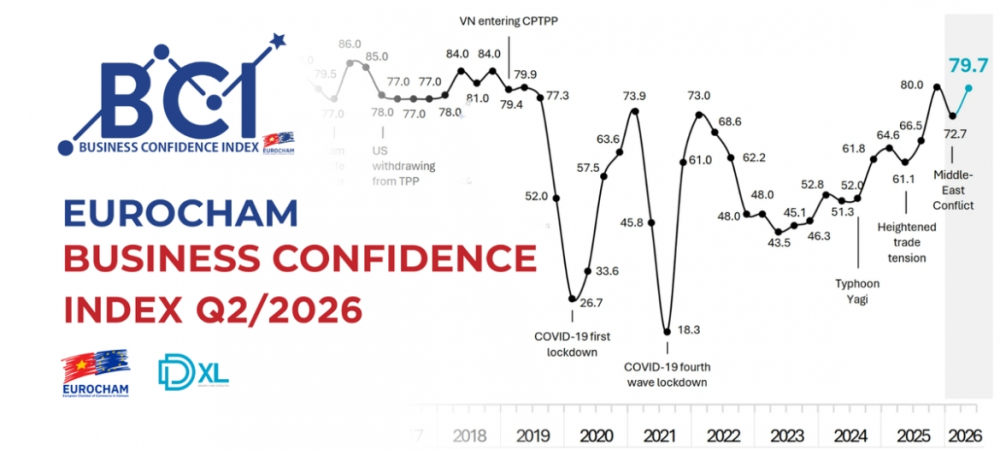

Business sentiment also strengthened. According to the NSO’s quarterly business survey, 85.2 per cent of FDI manufacturers expect business conditions in the third quarter to improve or remain stable compared to the second quarter. The corresponding figures were 82.8 per cent for private enterprises and 80.5 per cent for SOEs.

Expectations of rising production and stronger domestic and export orders have boosted confidence across industrial parks nationwide, encouraging businesses to invest in new equipment, improve production processes, and expand into new markets ahead of the year-end period.

Output growth eases inflation

The Manufacturing Purchasing Managers’ Index (PMI) provided further evidence of the sector’s improving health. According to S&P Global’s June 2026 Vietnam Manufacturing PMI report, released in early July, the Index rose to 51.8, signaling continued improvement in business conditions.

Manufacturing output expanded for a 14th consecutive month and at the fastest pace since the beginning of the year, supported by stronger inflows of new orders.

The report also pointed to easing inflationary pressures, with both input costs and output prices rising at their slowest pace in several months. Lower cost pressures have given manufacturers greater flexibility to maintain competitive pricing while protecting profit margins.

The moderation in inflation also reflects improving global supply chain conditions, though geopolitical tensions continue to create risks through higher shipping costs and occasional shortages of raw materials. Vietnamese manufacturers have demonstrated greater resilience by drawing on existing inventories and adopting more flexible procurement strategies.

Despite the broadly positive outlook, some challenges remain. Manufacturing employment declined for a fourth consecutive month even as production continued to increase, suggesting that companies still have spare production capacity or are relying more heavily on automation and productivity gains rather than expanding their workforce.

Outstanding workloads also declined sharply, indicating that factories are processing orders efficiently. The key challenge for the second half of the year will be translating higher production into sustained employment growth and a more resilient labor market.

Business confidence climbed to its highest level in four months, reflecting expectations of stronger global demand and continued investment in new product development. Hopes for a more stable international environment in the second half of 2026 are providing additional support for manufacturers’ expansion plans.

Mr. Andrew Harker, Economics Director at S&P Global Market Intelligence, believes Vietnam’s manufacturing sector ended the first half of 2026 on a positive note, with both new orders and output continuing to expand. Encouragingly, survey respondents attributed the growth primarily to improving underlying customer demand rather than precautionary inventory building.

At the halfway point of 2026, Vietnam’s industrial sector appears to be entering a new phase of expansion on increasingly solid foundations. Record IIP growth, the highest disbursed FDI in five years, and a steadily expanding PMI together underscore the sector’s resilience amid external uncertainty. Maintaining that momentum through the remainder of the year, however, will require effective policymaking and continued business adaptability to address logistics costs, localized labor shortages, and ongoing volatility in global markets.

Source: MANH DUC