Vietnam’s real estate market is likely to experience a great many changes over the course of 2026, with a host of factors coming into play.

Industry insiders believe 2026 will mark one of the most intense shakeout phases the real estate market has encountered in years. Compared to the early days of January, construction costs, including materials and labor, have risen by 15-20 per cent, while credit growth limits for the industry have been cut from 19 per cent to 15 per cent, with lending increasingly concentrated on large projects and major developers.

Mr. Nguyen Quoc Hiep, Chairman of the Vietnam Association of Construction Contractors (VACC) and Chairman of GP.Invest, told Vietnam Economic Times / VnEconomy that real estate companies will face fierce competition in 2026. “As a result, most smaller-capitalized property companies will continue to struggle with access to bank financing,” he continued. “Deposit rates have eased slightly, but lending rates remain at 11-14 per cent per annum. This has directly affected market liquidity. In the first quarter, at many projects, sales reached only around 30 per cent of levels seen in previous quarters, making profitability very difficult.”

Transactions down sharply

Ms. Do Thi Thu Hang, Senior Director of Advisory Services at Savills Hanoi, said mortgage rates at certain banks have climbed rapidly, at times reaching 15-16 per cent per annum. This has increased borrowing costs and directly affected both affordability and investment decisions.

For developers, she continued, elevated rates and tighter credit conditions have compounded financing costs and limited access to capital, particularly for less-viable projects. Only those with strong balance sheets, stable cash flows, and diversified fundraising channels have sufficient resources to continue project development and offer suitable interest rate support packages to buyers.

The market is entering a broad and forceful cleansing phase, she explained. Access to bank loans and investment funds will be scrutinized more carefully, with priority given to viable projects that meet genuine market demand. The divide between strong and weak players is becoming clearer than ever. While financially solid companies are using merger and acquisitions (M&As) to expand market share, weaker firms that relied heavily on leverage are stagnating.

On the buyer side, a “safe hands” approach would be directing attention toward developers with strong finances and proven reputations, while becoming more cautious in committing capital. Highly-leveraged investors, especially short-term speculators, face mounting risks as cash flow pressure may force distressed sales and market exits. This trend was quickly reflected in weaker liquidity and slower transactions in the first quarter of 2026.

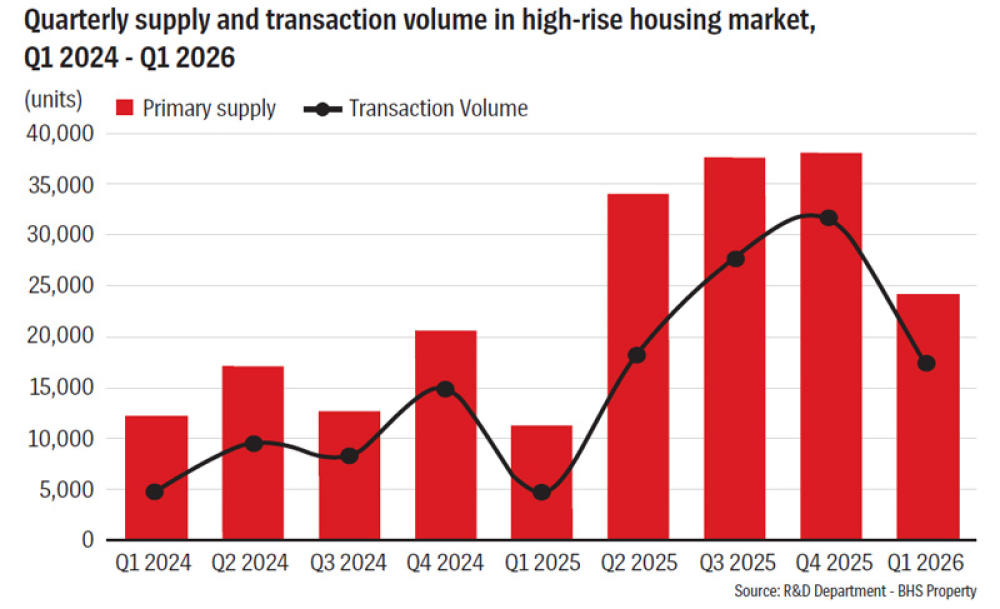

Ms. Pham Thi Mien, Deputy Director of the Vietnam Real Estate Market Research Institute (VARS IRE) at the Vietnam Association of Real Estate Brokers (VARS), citing the Institute’s latest report, said the market recorded around 24,000 transactions in the first quarter, equivalent to an absorption rate of 47 per cent of primary supply. The rate for new supply reached 58 per cent, or more than 22,000 transactions.

Compared with the previous quarter, absorption declined partly because the extended Lunar New Year (Tet) holiday fell in the first quarter and also because macro-economic volatility and persistently high borrowing costs made homebuyers more cautious. She added that projects priced more competitively than the broader market have recorded near-100 per cent absorption. Those with full legal documentation, reliable construction progress, and products serving genuine housing demand have maintained healthy liquidity, while those lacking infrastructure and amenities, especially land plots in many areas, remain subdued.

Six restructuring trends expected

Against that backdrop, Ms. Mien forecast that the market will be reshaped by six major trends over the remaining months of the year.

First, supply will be restructured through greater concentration and higher standards focused on green and sustainable development. Supply is expected to continue rising, but under the dominance of financially-strong developers with integrated execution capabilities. Large-scale township projects are likely to become the main source of new supply.

Second, development space will shift in line with infrastructure and integrated urban planning. Ring roads, expressways, and metro networks under Transit-Oriented Development (TOD) models are expected to see suburban areas and satellite cities become new growth poles.

Third, capital channels will be restructured as cheap money disappears. Developers are expected to reduce dependence on short-term leverage and move toward more sustainable funding structures, including higher equity contributions, joint ventures, M&A activity, and stronger project cash flow management.

Fourth, buyer behavior will become more practical, with decisions increasingly based on genuine utility and financial efficiency rather than expectations of rapid price.

Fifth, demand will be rebuilt on a more sustainable foundation, centered on genuine housing need in major cities and medium to long-term investment strategies.

Sixth, the market’s operating mechanism will become more polarized while moving toward sustainable standards. Capital and liquidity will be concentrated in projects with prime locations, full legal status, reliable progress, and reputable developers, while weaker projects will face growing difficulties in sales and fundraising, leading to natural market exits.

Meanwhile, the latest report from the Ministry of Construction (MoC) noted that, in the closing months of 2026, as new regulations are implemented in a coordinated manner and begin to take effect, the real estate market will continue to differentiate clearly and gradually move on to a more stable trajectory. Improved supply is expected to help stabilize overall pricing and curb unreasonable price increases, creating better conditions for genuine homebuyers.

Expert outlook

As the market moves deeper into restructuring, industry leaders believe the remainder of 2026 will be shaped by more selective demand, tougher competition, and a widening divide between stronger developers and weaker players. Affordable housing, infrastructure-led growth areas, and legally-sound projects are expected to remain key themes.

Ms. Hoang Thu Hang, Deputy Director of the Department of Housing and Real Estate Market Management at the MoC, said demand in the months to come is expected to focus on affordable homes, reasonably-priced condominiums in major cities, and land plots in areas with synchronized infrastructure and stable communities.

She added that brokerage activity is becoming more orderly and professional as tighter supervision and higher licensing standards come into being. Speculation and artificial price inflation will also face closer scrutiny, helping to curb abnormal market volatility. Meanwhile, greater transparency in market, planning, and policy information is expected to support buyers and investors.

Meanwhile, Mr. Le Xuan Nga, General Director of BHS Property, said the high-rise housing segment is projected to enter a broad supply expansion phase during 2026-2027, with more than 139,000 apartment units expected to launch, mainly from large-scale mega projects. However, he added that rising supply does not signal a return to overheated growth. Rather, developers are likely to face intensifying competition for liquidity and buyer attention.

To the end of the year, meanwhile, the low-rise housing segment is forecast to maintain positive momentum, with future supply exceeding 78,000 units, largely concentrated in mega urban developments with abundant land reserves controlled by major developers. Projects with stronger planning, legal clarity, amenities, and location are expected to outperform others.

Infrastructure investment is increasingly seen as the market’s most powerful long-term catalyst. Mr. Su Ngoc Khuong, Senior Director of Investment at Savills Ho Chi Minh City, said infrastructure is becoming the defining force reshaping the property landscape. Around 234 large-scale projects with total estimated investment of VND3,400 trillion ($130.8 billion) are underway, including Long Thanh International Airport, metro networks in Hanoi and Ho Chi Minh City, and more than 380 km of the North-South Expressway, which recently opened.

These projects are creating new economic corridors, supporting industrial real estate through integrated supply chain ecosystems while accelerating the rise of new growth poles in surrounding satellite areas.

According to Mr. Khuong, Vietnam entered 2026 from a position of growing strength, supported by stable macro-economic fundamentals, sustained FDI inflows, a more transparent legal framework, and an expanding interregional transport network.